Selecting the right health insurance plan is one of the most important financial choices people and families can make. Because of rising medical costs, hospital stays, and unexpected emergencies, having health insurance is no longer an option. People in India usually have to choose between private health insurance plans and government health insurance plans.

Both options help with healthcare, but they are different in terms of who can use them, what they cover, how flexible they are, how much they cost, and how easy it is to get to the hospital. Knowing the difference can help you choose the best plan for your budget, family size, and health needs.

We will compare both options based on key points. We will look at their cost, what they cover, and how much flexibility they offer. This guide aims to help you decide which plan suits your health and money needs best.

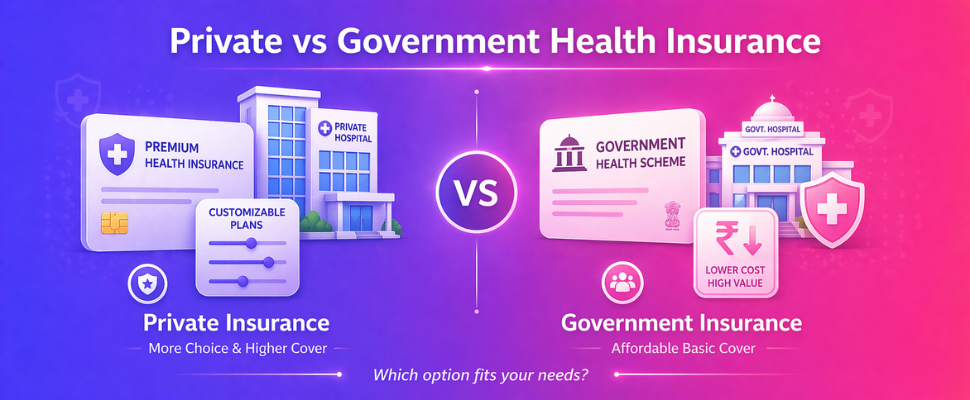

What Is Private Health Insurance?

A private health insurance plan is offered by private health insurance companies.Individuals can buy them directly. Employers also often provide them as group plans for their staff. When considering private health insurance vs public health insurance, these private options give policyholders more choice.

Typically, private health insurance policies provide coverage tailored to your specific needs. With such a plan, you can select your own doctors and private hospitals. This often leads to faster access to medical services. Understanding the operational differences is key when comparing private health insurance vs public health insurance.

These plans usually cost more each month compared to public options. However, you can change your benefits to fit what you need. For example, you can add coverage for a new baby or for dental visits. Private companies typically have large networks of private hospitals. This is a significant factor in the discussion of private health insurance vs public health insurance, as public systems often have different hospital access.

What Are Government Health Insurance Schemes?

Government health plans are paid for and run by the central or state government. Their main aim is to give basic healthcare that costs little or is free. These plans mostly help people in society who earn less money.

Ayushman Bharat (PM-JAY) is a key example. These plans typically have low or no monthly payments. To get them, you must meet specific rules about your income. Their network often works with public hospitals or those approved by the government. This helps explain private versus public insurance. Choosing between public or private health insurance depends on what each person needs.

Key Differences Between Private Insurance and Government Insurance

Knowing the main differences between private and government insurance is helpful. What is the main difference between private and government insurance? This section will compare private and government health insurance directly.

Private and government health plans show clear differences. Private options typically cost more. These costs depend on your age and overall health. Government plans, however, are often free or very cheap. Taxes usually pay for them. Private insurance gives full, personal coverage. Government plans mostly cover basic health services.

Private insurance lets you use many network hospitals. This often includes top private hospitals. Government plans usually limit you to public or specific approved hospitals. Anyone can buy private insurance if they can afford it. Government plans have special rules for who can get them. These rules are based on income or age. Private insurers generally pay claims faster. Government claims can sometimes take longer. Private plans offer more choices and extra options. Government plans are mostly the same for everyone.

Private Vs Government Health Insurance: Key Differences

| Feature | Private Health Insurance | Government Health Insurance |

|---|---|---|

| Premium | Paid by policyholder | Low-cost or free for eligible users |

| Eligibility | Open to most applicants (subject to underwriting) | Based on income, category, age, or scheme rules |

| Coverage Options | Wide range of customizable plans | Standardized scheme benefits |

| Sum Insured | Can be selected as per need | Fixed cover under scheme |

| Hospital Network | Private and network hospitals | Empanelled public and private hospitals |

| Add-ons | Yes (maternity, critical illness, room upgrades, etc.) | Usually limited |

| Renewal | Annual renewable policies | Depends on scheme rules |

| Tax Benefits | Usually available on premiums paid | Not applicable in same way |

Benefits and Limitations of Private Health Insurance

Benefits of Private Health Insurance

1. More choices for coverage

Depending on the insurance company, private plans may cover things like hospitalization, daycare procedures, ambulance charges, maternity benefits, mental health support, annual check-ups, and wellness rewards.

2. More options for higher sums insured

Depending on your health needs and where you live, you can choose plans that cover ₹5 lakh, ₹10 lakh, ₹25 lakh, or even more.

Confused between health insurance plans?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

3. Getting to private hospitals faster

Many private plans have big hospital networks that don't require cash, so you can get care at well-known hospitals.

4. Keeping your family safe

Family floater plans cover a spouse, children, and sometimes parents all under one policy.

5. Tax breaks

Under certain tax laws, you may be able to deduct the premiums you pay for health insurance.

Limitations of Private Health Insurance

- Requires premium payments every year

- Waiting periods may apply for certain illnesses or maternity

- Premiums may rise with age

- Policy wording and exclusions must be understood carefully

Benefits and limitations of government health insurance:

Knowing about government health plans matters. What are the pros and cons of government health insurance? These plans offer basic safety for many people.

Benefits of government health insurance

1. Coverage that is cheap or free

Most plans are meant to help families with less money pay less for medical care.

2. Hospitalization without cash

Eligible beneficiaries can get treatment at empanelled hospitals without having to pay a lot of money up front.

3. Coverage for Conditions That Already Exist

Some programs, like PM-JAY, say that people who are eligible will be covered for pre-existing conditions starting on day one.

4. Help from Social Security

Government plans help families get the care they need that they might not be able to afford otherwise.

5. Reach Across the Country

Many programs help people get treatment in more than one state by using networks of hospitals.

Confused between health insurance plans?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

Limitations of government health insurance

- Eligibility restrictions apply

- In big cities, fixed coverage might not be enough for expensive treatments.

- Few choices for customizing

- In some areas, there may be fewer hospitals to choose from.

- Package lists may only cover certain procedures.

How to Choose Between Private vs. Public Health Insurance

Choosing the right health insurance plan takes real thought. This section helps you understand, How do I choose between private and public insurance?. We will answer Which is better, government or private health insurance?. It will help you decide, Should I get private or public health insurance?. Here are key things to think about for private vs public insurance.

What medical care each plan covers

• Private plans often pay for more treatments and advanced hospital care.

• Government plans typically offer basic care with certain limits.

How much each choice costs you

• For those who qualify, government plans have very low or no monthly payments.

• Private insurance costs change based on your age, the sum insured, and features.

Which hospitals you can use

• Many private hospitals offer cashless service through private insurers.

• Government plans usually limit you to specific public hospitals.

How easily claims are paid

• Private insurers often give faster cashless claim options.

• Some government plans might involve more paperwork to get your money back.

Things to Compare Before Buying Any Plan

Whether private or government-supported, compare these factors:

Coverage amount

Network hospitals near you

Claim settlement process

Waiting periods

Room rent limits

Daycare coverage

Pre-existing disease terms

Renewal age limits

Confused between health insurance plans?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

- ## Customer support

Conclusion

Choosing between private and public insurance means looking at the good and bad points. Private health insurance typically covers many things. It usually offers more choices too. However, it often costs more money.

Government health plans, like Ayushman Bharat Yojana (PMJAY), help many people. They let them get important healthcare. Most can afford these plans.

Your best choice depends on what you need for healthcare. It also depends on how much money you have. What matters most to you is key. Consider your budget. Think about which hospitals

you prefer. Also, think about how much coverage you expect.

Making a smart health coverage choice is very important. It helps keep you healthy. It also protects your money for the future.

Frequently Asked Questions

Q1: What is the difference between a private and public insurance company?

The primary distinction lies in ownership. Public insurers, like LIC, are government-backed, typically known for extensive reach and traditional products. Private companies such as HDFC Life, however, are privately owned and you'll often see them focusing on innovation and technology-driven solutions. Both operate under IRDAI regulations (this can vary slightly in approach).

Q2: Which is better, public or private health care?

Neither is inherently "better"; it truly hinges on your personal needs and what you prioritise. Public schemes offer essential, affordable coverage, but typically come with specific eligibility and a narrower network (this can vary by state, of course). Private plans, from IRDAI-regulated companies, often provide more full benefits and higher sum insured options. You'll also get tax benefits under Section 80D.

Q3: Can I have both a private health plan and a government scheme at the same time?

You can certainly hold both a private health plan and a government scheme simultaneously here in India. Many find this dual coverage beneficial for a larger sum insured or wider hospital network (depending on the particular government program). You'll typically claim from one first, then the other plan can cover any remaining expenses.

Q4: Are pre-existing conditions covered differently in private vs. government plans?

Private plans typically have a waiting period for pre-existing conditions, often 2-4 years. Government schemes like Ayushman Bharat (PMJAY), however, usually cover these from day one for eligible beneficiaries (this can vary slightly by specific condition). It's always best you declare everything honestly during application, regardless of the policy.

Q5: Do I get tax benefits on both private and government health insurance plans?

You absolutely get tax benefits on premiums for both private and government health insurance plans. This deduction, under Section 80D of the Income Tax Act, typically covers policies from any IRDAI-regulated insurer (always check specifics). It's a great way to reduce your taxable income each financial year.

Q6: Is the claim settlement process faster with private insurance compared to government schemes?

Typically, yes, private insurance claims, especially cashless ones, tend to be faster due to advanced technology and larger network hospital tie-ups. While government schemes also aim for efficiency, their broader administrative structures might sometimes influence the timeline (this can vary by scheme). You'll find IRDAI mandates specific claim settlement periods for all private insurers.

Q7: Are there income limits for eligibility in government health insurance schemes?

Most government health schemes in India do have specific income or socio-economic criteria for eligibility. For instance, Ayushman Bharat PMJAY typically covers families identified through SECC data, which considers various income indicators. State-specific health schemes often set annual income limits to target Below Poverty Line (BPL) families or those with lower incomes; it's designed for those most in need (this often varies by state).

Q8: Who should buy private health insurance?

Working professionals, families, senior citizens, and anyone wanting higher coverage and broader hospital access should consider private plans.

Written By

Raj Shankar![]()

Principal Officer and General Manager at CoverTiger

With over 7 years of experience in the insurance and fintech industry, Raj Shankar has helped 10,000+ customers secure their families with the right insurance solutions. He has worked with leading brands such as Policybazaar, INDmoney, and CoverTiger, building strong expertise in health insurance, life insurance, sales leadership, and customer advisory. His mission is to make insurance simpler, more transparent, and accessible for every Indian family.