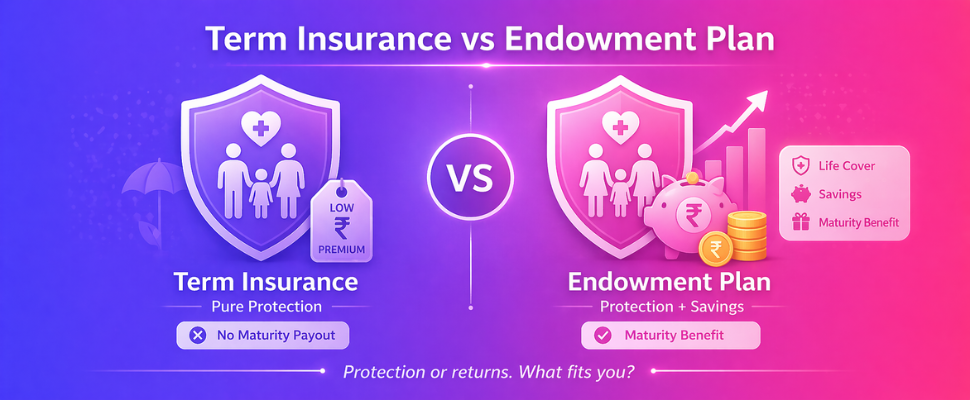

Selecting life insurance is a major decision that influences your family's security for decades. You'll need to cover your debts. Most people look at two specific routes, term insurance or endowment plans. Term insurance pays a death benefit only. It is the cheapest way to buy a high level of protection because there isn't an investment element. Monthly costs stay low.

Endowment plans operate differently by blending life cover with a way to build wealth.

If you outlive the policy, the insurer sends a payout. This breakdown of term insurance vs endowment plans skips the sales pitch to help you compare prices and decide which one fits your life.

Key takeaways

Keep a few basic facts in mind.

- A term insurance policy focuses on death benefits so you can afford much higher coverage. You won't get money back if you outlive the policy term.

- Endowment plans offer a mix of life cover and savings. The insurer pays out money when the policyholder dies or the plan matures.

- Match your choice to your financial goals. Pick term plans for pure protection. Use an endowment plan if you'd like to grow wealth.

- Premiums for term insurance are much lower. This is because endowment costs include a part that builds a cash fund along with the insurance.

- Both choices offer tax benefits. You can claim deductions on premiums and get tax-free payouts under Section 80C and 10(10D) by following the rules.

What is term insurance?

Term insurance is a basic safety net for a family. Under these contracts, the insurer pays a lump sum to beneficiaries if the policyholder dies.

- Coverage stays active for the exact duration you choose at the beginning of the plan.

- Within that defined window, a payout only happens if death occurs.

- You usually won't get money back if you're still living once the policy ends.

- Premiums stay affordable even for large payouts.

What is an endowment plan?

Endowment plans are a hybrid of life cover and a savings tool. These policies pay out regardless of whether you've passed away or live to see the term end.

- If you die before the plan matures, the insurer pays your family a death benefit, but surviving means you'll get a maturity payout.

- Total amounts often include the base sum plus bonuses, though specific figures change between products.

- Many use these to pay for a child's school fees or to build a retirement pot.

- Premiums are usually more expensive than term insurance because the company invests to guarantee that final lump sum.

Term insurance vs endowment plan: a head-to-head comparison

Thinking about your future involves comparing specific features to see which policy fits best.

Primary goal

A term plan is designed to provide your family with a financial safety net. If you pass away during the policy years, your loved ones receive a payout. It is a simple way to protect them.

Endowment plans work toward two goals by providing life insurance cover while helping you save money in a disciplined way. You get the benefit of protection and a lump sum later. This helps with your long term financial planning and provides a bit of a reward for staying with the policy until the end.

Premium cost

Not sure how much term cover you need?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

When you compare prices, you'll see that term plan premiums are usually much lower. This makes it easier on your wallet. You can get a high level of cover without spending too much.

Why does an endowment plan cost more? It is because some of your money goes into a savings pot rather than just paying for the insurance itself. The cost reflects the dual nature of the policy. Most people pay a higher premium for this mixed benefit.

Benefits payout

This type only pays out a death benefit to your nominees. There is no money back if you outlive the policy term. It is purely for protection during the years you need it most.

You receive a death benefit if you pass away during the term, but you also get a maturity payout if you reach the end of the term. This survival benefit is a big part of the appeal for many. Check the specific terms for any bonuses.

Sum assured

For a relatively small premium payment, you can secure a very high amount of coverage for your family.

The sum assured usually stays lower for the same price point because your money is split between insurance and savings. You are paying for the savings component as much as the life cover. This means you might need a separate policy if you want a massive payout for your heirs.

Risk and returns

There is no investment side here. You face no market risk and you do not get any financial returns on the money you pay. It is a simple service fee for a guaranteed payout.

These are low-risk investments that offer modest or even guaranteed returns on your money over the long haul. They often include bonuses that the company declares every year. Because the returns are tied to the insurer's performance, they are usually quite stable.

Liquidity

You won't find any liquidity here since the policy has no cash value and you cannot surrender it for money. Once you stop paying, the cover usually just ends with no value left. It is not an asset you can tap into for cash.

After several years of paying, your policy might offer a surrender value, letting you take out loans or withdrawals if you need money. This gives you a bit of a safety net for emergencies.

Tax benefits

You can deduct your premiums under Section 80C, and your family usually gets the death benefit tax-free under Section 10(10D). It is a tax-efficient way to protect your income.

Both your premiums and the final payouts are eligible for tax breaks under Section 80C and Section 10(10D), though you must follow specific rules to qualify. This applies to both the death and maturity benefits. Make sure your annual premium is not more than ten percent of the sum assured.

| Feature | Term Insurance | Endowment Plan |

|---|---|---|

| Primary goal | This plan focuses on protecting your family if you pass away during the policy years. | It offers protection plus a savings payout if you survive until the end of the term. |

| Premium cost | You pay much lower premiums for the same level of insurance cover. | Premiums are higher because part of the money builds up a savings fund. |

| Benefits payout | The plan pays a death benefit only, with no payout if you survive the term. | You get a death benefit on a claim or a maturity benefit if you survive, often with bonuses. |

| Sum assured | You can usually get a higher sum assured for a very low premium amount. | The sum assured is lower for the same price because some money goes to savings. |

| Risk and returns | There is no investment risk involved and you do not get any returns. | Returns are usually low to moderate and can include guaranteed additions. |

| Liquidity | There is no cash value here and you cannot surrender the policy for money. | You can get a surrender value or a policy loan after the lock-in period ends. |

| Tax benefits | You can deduct premiums under 80C, and death proceeds are typically tax-free under 10(10D). | Both your premiums and the final payouts can get tax benefits under 80C and 10(10D). |

Not sure how much term cover you need?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

Which plan fits your financial goals, term insurance or endowment?

Picking between a term plan and an endowment plan is not about finding the superior option. It's about what makes sense for your lifestyle. Where do you see yourself in a decade? Risk and budget matter as much as age. Often, the choice is whether you want a safety net or a savings vehicle.

When should you choose a term insurance plan?

Buying pure protection is the main attraction for most people. A term insurance plan typically works best if you want high coverage without a high price tag.

- Protecting your family with a massive payout is a top priority, but you want to keep monthly premiums affordable.

- If you have a large mortgage or student loans, your relatives will need a way to settle those specific debts.

- Cash might be tight today, yet you still want to ensure a death benefit stays in place for safety.

- Investing works better for you through stocks or mutual funds, so you prefer to keep your life insurance and wealth building completely separate.

When should you choose an endowment plan?

These policies work for people who want low-risk savings. It's a disciplined tool.

- Rigid savings schedules help you prepare for a specific milestone, such as a child heading to university in exactly fifteen years.

- Market volatility is something you want to avoid, so you prefer staying away from the stock market.

- Funding a future wedding or even your retirement is much easier when there is a guaranteed lump sum payout waiting for you.

- Because your basic life cover is already in place, you may just want a low-risk place to put your surplus funds.

How cover tiger helps you compare term insurance vs endowment plans

Identifying your specific needs comes first.

Market comparison is non-negotiable because policies with similar names often hide different rules in the fine print. It is usually wise to check claim settlement ratios alongside riders and exclusions. Surrender rules and premium structures also vary. Cover Tiger simplifies this by asking about age, liabilities, and goals. The platform then presents options from various insurers so you'll see premiums and sum assured side by side. Facts drive the choice, not sales pressure.

Transparency helps you spot the details that matter. For instance, you can see if a term plan includes critical illness riders or how an endowment plan calculates terminal bonuses. Because surrender values aren't always clear, seeing the math helps you decide if a pure term cover or a hybrid endowment plan fits your future.

Conclusion

Term insurance provides straightforward protection that stays affordable for most people today. It offers a way to secure a financial safety net for your family without the extra cost of savings features or payouts at the end. Alternatively, endowment plans mix life cover with a mandatory savings component. This means you receive a lump sum if you survive the policy term, though the premiums are usually much higher as they cover both life insurance and savings together in one plan.

No single choice is always best.

Typically, a term plan works for those who need large cover on a budget. If you want to build wealth while staying insured, an endowment plan could work. Think about your debts and the financial gap your family might encounter later.

Check various plans using an online tool. Review the riders and the fine print before deciding. This ensures the policy doesn't fail.

FAQs

Not sure how much term cover you need?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

1. Which is better, term insurance or endowment plan?

Your choice will depend on what you need your money to do. For those who want the biggest possible payout for their family at the lowest cost, term insurance is often the right move. On the other hand, an endowment plan works for people who need to be forced into a savings habit while keeping their life cover active.

2. What is a disadvantage of term insurance?

The main catch with these policies is that you get nothing back if you outlive the term. Since there is no maturity benefit, the premiums you paid over the years stay with the insurer. They are strictly for protection and do not build cash value. It's a "use it or lose it" scenario.

3. What are the disadvantages of an endowment fund?

You'll probably notice that the costs for these plans are much higher than what you'd pay for term insurance. This is because the company has to manage a death benefit and a savings pool simultaneously. Often, the returns end up being fairly modest. They usually fall below what you might earn by putting that same money into stocks or mutual funds. Flexibility is another issue. If you need your cash early, you might run into strict lock-in periods or face heavy fees for taking money out.

4. Can I withdraw my endowment policy?

Yes, but it is not something you can do right away. Most insurance companies will require you to pay premiums for at least two or three years before the policy builds any surrender value. Once that milestone is reached, you have the option to take a loan against the balance or cancel the policy for a payout.

5. Is an endowment plan considered a good investment?

Whether this is "good" depends on your appetite for risk. If you prefer guaranteed safety over aggressive growth, an endowment plan offers a steady way to build wealth while keeping life cover active. But if you want your money to grow faster over several decades, equity-linked products or mutual funds usually do a better job of hitting those long term goals.

6. Do I receive both a death benefit and a maturity benefit from an endowment plan?

You do, but you usually won't get both at the same time. If the person covered passes away during the term, the company pays the death benefit to the family. If that person survives until the plan ends, the company pays the maturity benefit instead. It is a dual-purpose setup that covers both outcomes in one policy.

7. How much life cover should I get with a term insurance plan?

Most people aim for a payout that is roughly 10 or 15 times their annual salary. While that's a good starting point, you also need to factor in your specific debts like a mortgage. Getting the right amount ensures your family can maintain their current lifestyle.

8. What happens if I stop paying the premiums for my endowment plan before it matures?

Missing a single payment doesn't mean the policy is canceled immediately, as most insurers give you a grace period. If that time passes and you still haven't paid, the policy might lapse. This means you lose your life insurance cover entirely. For policies that have been active for many years, the insurer might turn it into a "paid-up" plan. In that case, your benefits are reduced but the policy stays active. Just know that walking away early almost always leads to lower returns and the loss of any bonuses you have built up.

Written By

Raj Shankar![]()

Principal Officer and General Manager at CoverTiger

With over 7 years of experience in the insurance and fintech industry, Raj Shankar has helped 10,000+ customers secure their families with the right insurance solutions. He has worked with leading brands such as Policybazaar, INDmoney, and CoverTiger, building strong expertise in health insurance, life insurance, sales leadership, and customer advisory. His mission is to make insurance simpler, more transparent, and accessible for every Indian family.