Life insurance offers vital financial protection for your family. Most people know about standard term insurance. However, other specific plans can suit different money needs.

Decreasing term insurance is one such plan. It covers debts that naturally get smaller over time, like a home loan. This insurance helps manage decreasing liabilities at a lower cost.

This guide explores decreasing term insurance. It shows how the plan works, its benefits, and who might find it useful.

What Is Decreasing Term Life Insurance?

Decreasing term life insurance is a special type of life cover. The death benefit slowly gets smaller. This happens over the policy's term. But premiums usually stay the same. This drop follows a clear plan. This policy helps fit money to family needs. It often pays for debts that get smaller, like a home loan. Many people also call this reducing term life insurance.

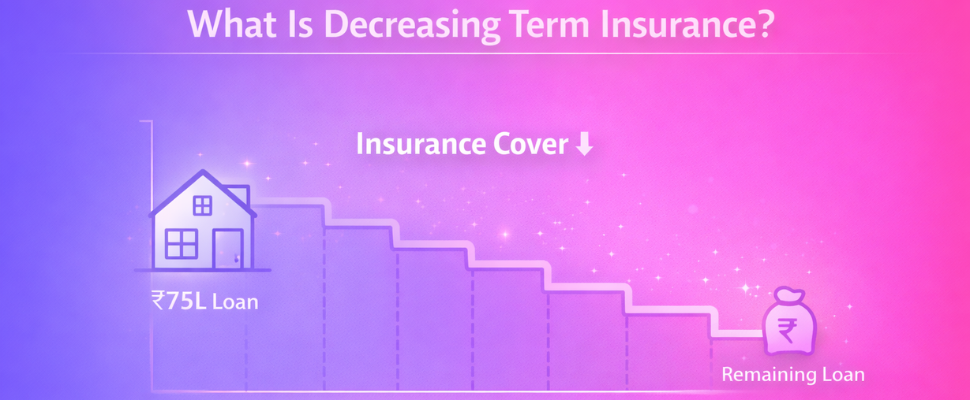

How Does a Decreasing Term Plan Work?

Decreasing term insurance gives you cover that gets smaller over time. Here's how decreasing term insurance works. The sum assured, or cover amount, goes down on a fixed plan. Typically, it reduces each year. The policy's payout matches your falling financial needs.

For a clear policy example, think about a home loan. Someone takes a ■75 lakh home loan for 25 years. They buy a 25-year decreasing term insurance policy. The starting cover is also ■75 lakh. If a claim happens in year 5, the payment covers the remaining loan. Should it happen in year 20, the payout will be much smaller. It will match the much lower loan amount still owed. This direct link offers good mortgage protection. It also stops you from paying for too much cover later on. This plan is often very affordable.

Key benefits of a decreasing term policy

This policy helps with specific money needs. Decreasing term insurance offers several benefits, making it a good choice for many people.

Debt Protection: This insurance helps keep your family safe from loans you still owe. The amount of cover slowly drops as your loan balance gets smaller. This can help your loved ones pay off debts, like home loans.

You often find this policy costs less than a regular level term plan. The initial cover amount reduces over time, which usually means lower premiums for you. It's a way to get life insurance that costs less for many Indian families.

Matches Your Money Needs: This type of policy aligns with your financial responsibilities as they decrease. When your duties get smaller, your insurance cover does too. You only pay for the protection you actually need at that time.

Not sure how much term cover you need?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

You can get tax benefits from the premiums paid for decreasing term insurance. These typically fall under Section 80C of the Income Tax Act, 1961. Also, money paid to your family is usually tax-free under Section 10(10D).

Lower premium costs

Decreasing term insurance offers you life cover. The money it pays out gets smaller as the policy goes on. Premiums for this kind of plan are often lower than for regular term plans. This makes it a smart choice for many Indian families looking to save money. The possible payout amount reduces over time. This reduction matches how your financial debts go down. For instance, the cover amount shrinks with your home loan or car loan. This plan offers life protection that you can truly afford. People who buy these policies typically find premiums stay fixed for the whole policy time. This keeps your costs clear for the entire duration you have the policy.

Tailored debt repayment

Decreasing term insurance is a unique type of life cover. It helps pay off your unpaid debts over a set time. The money paid out from this plan gets smaller each year. This reduction often matches how your loan balance goes down. This setup makes sure your family avoids big financial burdens. These could be home loans or business loans. The plan gives your family important financial safety if something unexpected happens to you. This kind of plan usually costs less than a regular level term plan for the same starting cover.

Tax advantages

Decreasing term insurance can help protect your home loan. This plan makes sure the sum assured gets smaller as your loan amount reduces. It typically matches how much you still owe. This setup often means your yearly payments might also decrease. People holding this policy can get tax benefits under Section 80C on the payments they make. If something happens, the death benefit paid to your nominee is tax-free under Section 10(10D). This gives your family financial safety, easing the burden of loan repayment.

Which is right for you, decreasing term or level term insurance?

Level Term Insurance gives a fixed death benefit. This amount stays the same during your policy term. The main difference between term plans is how the money changes over time. When you consider decreasing vs level term insurance, remember this key idea.

Your choice often depends on your specific financial need. For instance, if you want to cover a debt that reduces, like a home loan, decreasing term insurance typically works well. If your goal is to provide constant support for your family, a level term plan might be a better fit. This is the core difference for term decreasing life insurance.

Who should consider a decreasing term plan?

Decreasing term insurance is not for everyone. It suits people with specific money responsibilities. This plan works well when you want to cover a debt that shrinks over time. Knowing who needs decreasing term insurance can help your family's financial future.

Home Loan Borrowers

Not sure how much term cover you need?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

If you have a home loan, this policy offers focused protection. As you pay off your loan, the amount covered by your decreasing term plan also goes down. This helps your family settle the remaining home loan amount without worry. Many people call it mortgage life insurance. It directly covers your debt.

Business Loan Borrowers

Business owners often take loans to help their companies grow or run daily. A business loan insurance plan protects your company if the main earner passes away. This decreasing life term insurance ensures the business debt gets paid. It stops financial problems for partners or family members.

People with Other Large Debts

Those with car loans, education loans, or big personal loans can also find this useful. The policy’s coverage matches your debt as it decreases. This gives clear financial protection for your family from specific debts. It helps avoid passing on a money problem to your loved ones.

Homeowners with a repayment mortgage

This is a common way to use decreasing term insurance. It helps your family pay off the home loan balance. This ensures they can keep their home if something happens to you.

Business owners with business loans

Business partners often use decreasing term insurance. This plan helps safeguard their business loans. If a partner dies, the company can keep running without financial stress for the others.

Individuals with other significant personal loans

People with long-term car or education loans might consider decreasing term insurance. This plan helps pay off specific personal debts. Your insurance money gradually matches your shrinking loan amount.

Conclusion

Decreasing term insurance offers an affordable way to get coverage. It covers specific debts that shrink over time. This type of plan works well for homeowners with home loans. Business owners also use it for paying off certain loans.

Not sure how much term cover you need?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

However, for daily family costs or replacing income, level term insurance is typically a better choice. Your personal financial plan must fit your exact needs. Carefully check your financial debts and long-term goals. This helps you choose life insurance wisely. Make a smart term insurance decision.

Frequently Asked Questions

Can I discontinue my term life insurance policy?

You can discontinue your term life policy by simply stopping your premium payments. It'll lapse, and your life cover stops immediately. Unlike some traditional plans, term insurance doesn't typically accrue any cash value, so you won't get any money back (this is standard for pure protection plans). Just remember, your family loses that critical financial safety net then.

Can you reduce term life insurance?

You can, but it's typically through a specific product called 'decreasing term insurance' in India. This plan lets the sum assured reduce over time, usually matching a diminishing liability like a home loan (this isn't an option for a standard term policy). It provides coverage that aligns with your decreasing financial commitments.

What happens to my policy if I pay off my mortgage early?

Your decreasing term policy continues as per its original schedule, even if you pay off your mortgage early. That sum assured still reduces over time regardless of your current loan status (check with your insurer). Typically, it's a good idea to review the policy document and discuss its future utility with us.

Can the death benefit decrease to zero before the policy ends?

Yes, in decreasing term plans, the death benefit can certainly become zero before the policy matures. This type of plan is typically designed to align with a diminishing liability, like an Indian home loan, so the cover reduces over time. If that underlying loan is fully repaid (check with your bank), then the remaining sum assured won't be there, having served its purpose.

Does decreasing term insurance have any cash or surrender value?

Decreasing term insurance carries no cash or surrender value. It's designed purely for protection, where the sum assured typically reduces over the policy term to align with a decreasing liability like a home loan (this can vary). You won't accumulate any savings component here.

Written By

Raj Shankar![]()

Principal Officer and General Manager at CoverTiger

With over 7 years of experience in the insurance and fintech industry, Raj Shankar has helped 10,000+ customers secure their families with the right insurance solutions. He has worked with leading brands such as Policybazaar, INDmoney, and CoverTiger, building strong expertise in health insurance, life insurance, sales leadership, and customer advisory. His mission is to make insurance simpler, more transparent, and accessible for every Indian family.