It is important to know how to figure out the cost of health insurance. A health insurance premium is your regular payment. This keeps your policy active and ensures you have health coverage. Many wonder: how do Indian insurance companies set this price?

This guide will help explain how to calculate health insurance premium. We will look at the main things insurers consider. These often include your age, the amount you are insured for (sum insured), and your past health. Online premium calculators can make getting an idea of your insurance costs much simpler.

What is a health insurance premium?

A health insurance premium is the regular fee you pay to your insurance company. This payment keeps your health coverage active. It forms your policy cost. Also, it helps protect you from significant medical expenses.

Often, people confuse the health insurance premium with a deductible or a co-pay. Premiums ensure you can use your health plan. You usually pay a deductible or co-pay when you get medical services.

It is important to understand how insurers calculate health insurance premium. This knowledge helps you plan your finances better. Knowing how to figure out medical insurance premium is also useful. You typically pay premiums every month or year.

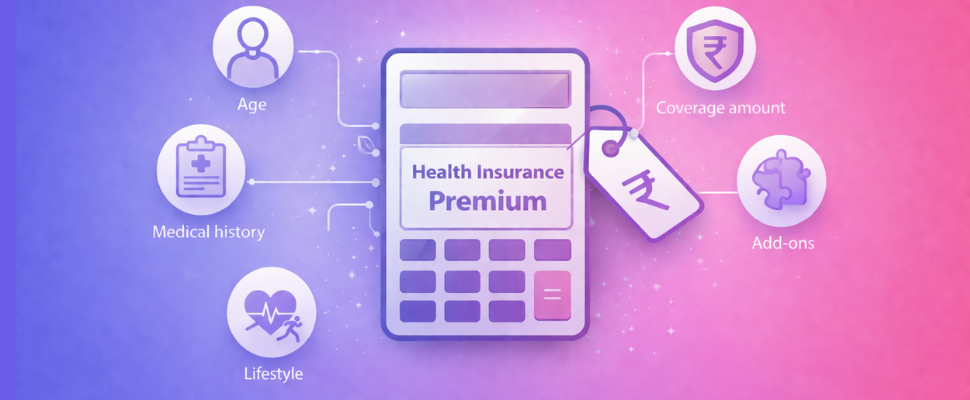

Factors that decide how your health insurance premiums are calculated

Insurance companies in India look at several things to calculate health insurance premiums. These points help them guess how likely you are to need medical care. Understanding them helps you choose a good plan.

Your Age

How old you are is very important. Younger people typically pay less money. This is because they often have fewer health issues. As you get older, your chance of health problems increases. This makes your premium higher.

Medical History

Your past health plays a big role. Any health problems you already have, such as diabetes or high blood pressure, will change your premium. They adjust the premium based on these issues. This is a key part of their risk assessment.

Lifestyle Choices

Your daily habits also change the cost. Smoking, drinking alcohol, or not being active can make your premium go up. These choices usually mean you have a higher chance of future health problems.

Sum Insured and Coverage Type

Confused between health insurance plans?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

The amount of coverage you pick directly affects the premium. A higher sum insured means you will pay more. The type of plan matters too. An individual plan costs differently from a family floater. Family floater plans cover many people, which changes their premium calculation.

Deductibles and Co-payments

Choosing a higher deductible or co-payment can lower your premium. A deductible is an amount you pay yourself before the insurer covers costs. A co-payment is a part of the bill you pay. These choices help reduce the company's initial payout.

Riders and Add-ons

Adding extra benefits, called riders or add-ons, increases your premium. Options like critical illness cover or maternity benefits make your plan better. However, they also add to the total cost. All these factors affecting health insurance contribute to the final price.

How to calculate health insurance premium

A simple way to calculate your health insurance premium involves using an online tool. These health insurance premium calculators take your personal details. They then quickly estimate your cost based on key factors. An online premium calculator provides a fast, custom quote. You can easily figure out your health insurance premium this way.

To use the Cover Tiger online premium calculator, take these steps:

1. Give your basic details. This includes your age, current city, and how many family members need cover. You might also mention if anyone has a health problem already.

2. Choose the coverage you want. Pick the sum insured amount you need. Also, select the policy type, like individual or family floater plan.

What's the formula for how insurance premiums are calculated?

How insurance companies calculate health insurance premium is not set by one public rule. However, a simple model shows the main parts. Insurance companies typically follow this plan:

Base Rate + Loadings - Discounts = Final Premium

• Base Rate: This forms the core price. It changes based on your age, where you stay, and the benefits in your chosen plan.

Confused between health insurance plans?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

• Extra charges are known as Loadings. These apply if you have higher risks, like using tobacco. Picking more add-on benefits also makes this amount go up.

• Discounts: These reduce how much you pay. For instance, a No Claim Bonus can lower the cost after one year without claims. Some Indian companies offer discounts if you agree to co-payment.

This helps you understand the premium costs from an online premium calculator.

Tips to calculate medical insurance premium savings

When you calculate health insurance premium, some things are fixed, like your age. Yet, you can often find ways to reduce health insurance premium. These simple steps help lower insurance costs. You can truly save on health insurance over time.

Increase Your Deductible

Choosing a higher deductible typically lowers your yearly payment. A deductible is the amount you pay first. Your insurance company starts paying after that. For example, a plan with a Rs. 15,000 deductible will cost less. It will be cheaper than a plan with a Rs. 5,000 deductible. This is a clear way to spend less on your payment.

Consider a Co-payment Option

Some plans offer a co-payment rule. This means you pay a fixed part of each bill, like 10% or 20%. Picking a plan with co-payment can make your payment much cheaper.

Use Your No Claim Bonus (NCB)

The No Claim Bonus (NCB) rewards you for not making claims in a policy year. Your insurance company, like Star Health or ICICI Lombard, increases your sum insured without raising your payment. Alternatively, they might give you a discount on your next payment. This really helps you save on health insurance.

How to compare plans and find out how insurance premiums are calculated

Choosing health insurance plans needs careful thought. Do not just look at the lowest premium. It is wise to compare the coverage, available network hospitals, and policy benefits. A very low premium plan often gives less protection. Your past medical history and current health issues can greatly affect costs.

Cover Tiger helps you calculate health insurance premiums correctly. Our platform offers fair suggestions. We show the right balance between premium and full coverage. This includes

looking at many policy types.

Use Cover Tiger to compare custom quotes from good insurers. Make a smart choice without any sales pressure. This helps you pick the best value for your family's health needs.

Confused between health insurance plans?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

Conclusion

Many personal factors influence your health insurance premium. Your age, where you live, and the policy you pick are important. The size of your family also matters. Even your lifestyle choices can change the final cost.

However, you can adjust your premium amount. For instance, choosing a higher deductible often saves you money. When you choose health insurance, comparing plans carefully is very important.

To get a clear summary of your health insurance premium, use an online premium calculator. These are our final thoughts on how to calculate your health insurance premium correctly.

Frequently Asked Questions

Q: How much premium for 2 lakh health insurance?

For a Rs. 2 lakh health plan, premiums typically depend quite a bit on your age and health profile. A healthy person in their 30s might pay roughly Rs. 5,000 to Rs. 8,000 annually, though this figure can vary. It's always best to compare quotes from different IRDAI-regulated insurers, as each has its own pricing structure (you'll see differences).

Q: Does my No Claim Bonus transfer if I switch insurance providers?

Yes, your No Claim Bonus (NCB) typically transfers when you switch health insurance providers. The IRDAI allows for this portability, so your new insurer will consider your accumulated NCB.

You'll simply need to provide a No Claim Bonus certificate from your previous company (this is crucial for processing).

Q: Will my premium be higher if I have a pre-existing condition like diabetes?

Your premium will typically be higher if you have a pre-existing condition like diabetes. Indian insurers assess that added risk, often applying a loading—an extra charge—or a waiting period before your coverage starts (this can vary by plan). The exact premium increase really depends on the condition's severity and the specific insurer; it's always good to compare.

Q: Is it always better to choose a policy with the lowest premium?

No, focusing just on the lowest premium isn't always wise. Cheaper plans typically mean less coverage or higher out-of-pocket costs later (like co-payments). You'll want to evaluate benefits and the hospital network (especially for major Indian cities), ensuring it genuinely meets your family's healthcare needs.

Written By

Raj Shankar![]()

Principal Officer and General Manager at CoverTiger

With over 7 years of experience in the insurance and fintech industry, Raj Shankar has helped 10,000+ customers secure their families with the right insurance solutions. He has worked with leading brands such as Policybazaar, INDmoney, and CoverTiger, building strong expertise in health insurance, life insurance, sales leadership, and customer advisory. His mission is to make insurance simpler, more transparent, and accessible for every Indian family.