Good health insurance matters a lot for Indian families today. Healthcare costs are going up across the country. Experts suggest medical inflation could hit 11.5% to 14% by 2026. A basic health insurance plan is often not enough for big medical bills because of this.

Many people with insurance look to make their current coverage better. Cheaper choices like top up health insurance and highly top up health insurance are available. These plans offer extra money protection above your main base policy.

It is wise to know the difference between top up and highly top up health insurance. This guide will show how each works. It helps you pick the best choice for your health needs.

What is a top-up health insurance plan?

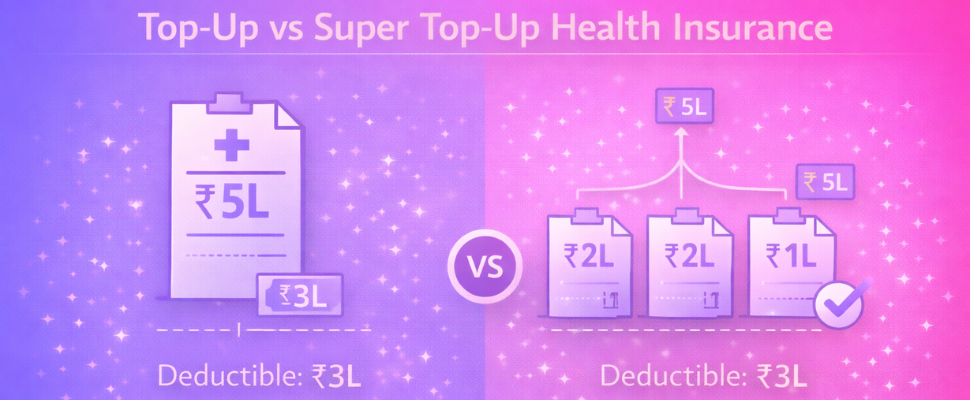

A top-up health insurance plan gives you extra coverage. It adds to what your current policy offers. This plan pays medical bills only after a fixed deductible amount is met. Typically, this deductible applies to each single claim.

For instance, imagine your deductible is 3 lakh. If your hospital bill is 5 lakh, the top-up plan will pay the extra 2 lakh. However, if another claim in the same year is 2.5 lakh, the top-up plan may not start. This is because the claim amount is less than the deductible for that specific event. This plan helps increase your total coverage. It protects you against large, single medical costs. Many Indian insurers offer this as a type of highly top health insurance, but it differs from a full highly top-up health insurance plan.

What is a super top-up health insurance plan?

A highly topup health insurance plan offers extra coverage. It begins paying once your total hospital bills in a policy year go over the deductible amount. This plan uses an aggregate deductible. It adds up all your cumulative claims for that policy year.

For example, imagine a 3 lakh aggregate deductible. If you have two hospital bills, each for 2.5 lakh, your total claims reach 5 lakh. The highly top up health insurance plan typically covers the 2 lakh excess. This provides wider financial help for multiple hospital stays.

Difference between top-up and super top-up health plans:

Top-up and highly top-up health plans both give you important extra money protection. They add to what your current health plan covers. Knowing the Difference between Top-up and highly Top-up Health Plans is very important. This helps you pick the right plan for your needs. The biggest difference is how their deductible works.

A top-up plan applies its deductible to each claim you make. This means you meet the deductible every time you claim. For a highly top-up health insurance plan, the deductible works differently. It combines all claims made in one policy year. The highly top-up plan typically starts to pay once your total claims reach the deductible amount.

Later, we will share a full table. It will clearly explain the details of Top Up Vs highly Top Up Health Insurance. This table shows the main differences. These points include how claims are settled and how premiums are decided. The next sections will talk more about these key points.

Confused between health insurance plans?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

| Parameter | Top-up | Super Top-up |

|---|---|---|

| Deductible Type | Per claim (each hospitalization) | Aggregate, per policy year |

| Claim Coverage | Activates only if an individual claim crosses the deductible | Activates once total claims in the year exceed the deductible |

| Ideal for | Young, healthy individuals who want protection against a single large event | Families, senior citizens, people with chronic or recurring medical needs |

| Premium Cost | Generally lower | Slightly higher, but often better value if you face multiple claims |

How the deductible gets applied

A regular top-up plan makes you pay its deductible for each hospital stay. This means you pay the deductible every time you ask for money. However, a high top-up health plan works differently. Its deductible covers all claims within one policy year. This usually gives you better money safety.

• You only pay the deductible once each policy year.

• Covers many claims after you meet the total deductible amount.

• Gives more money protection for many hospital visits.

Coverage scope for multiple claims

A regular top-up plan only pays if one claim crosses the deductible. It does not combine smaller bills. highly topup health insurance pays for all claims in one policy year.

• It starts paying after all your claims together pass the yearly deductible.

• This protects you from many small hospital stays.

• The deductible applies just once for all events.

Premium costs

Top-up plans typically have lower premiums. This is because the deductible applies to each new claim. In contrast, a super topup health insurance plan applies the deductible only once per policy year. This offers better value if you expect multiple claims within a year. A highly topup health insurance plan, similar to a super top-up, also provides comprehensive cover for multiple hospital stays after the deductible is met.

• Top-up plans give lower premiums per single claim.

• Get better value with super topup health insurance for many claims.

How does a deductible work in these health plans?

With extra health insurance, the deductible is the first amount you pay for medical bills. Your insurance company starts paying after you pay this amount. You can pay this money yourself; this is called "out-of-pocket." Or, your regular health insurance plan might pay it.

Usually, if you pick a higher deductible, your extra health insurance plan costs less. It is key to choose a deductible amount that matches your regular plan's insured amount. This helps make sure you have full coverage for your medical needs. An aggregate deductible can also help you control your total yearly costs.

Top-up or super top-up health insurance: which plan is better for you?

Confused between health insurance plans?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

Picking the right health insurance plan, like a top-up or highly top-up, depends on your health and budget.

When to choose top up You might choose a top-up plan if your main health coverage has a high sum insured. This option usually works best if you foresee only one big hospital bill in a year. The deductible applies to each separate claim. If just one major medical issue goes over your main plan's limit, a top-up can help. It offers extra cover and saves money. This helps with big rises in medical costs.

When to choose highly top up It is often better to choose a highly top-up if you think you will have many claims during a single year. This plan sums up all medical costs after the deductible is met. For instance, if you get several smaller hospital bills that add up, the highly top-up health insurance will cover them. This starts once the total deductible is crossed. This plan gives you full coverage for all your medical bills combined. It provides stronger financial safety for different health needs throughout the year. Consider your family's health and future medical costs when you pick a health insurance plan.

How to compare and choose the best super top-up plan with Cover Tiger

Finding the best highly topup health insurance needs careful thought. Cover Tiger offers an AI-powered comparison platform. This tool helps you easily compare health insurance plans from many companies. You can find the best top-up plan that suits your budget and needs. It ensures you choose well, without sales pressure. Use Cover Tiger for simple options to get financial

security.

Conclusion

A highly topup health insurance plan provides strong financial protection. Its special cumulative deductible often gives wider coverage. This is key because medical costs typically keep rising.

Your health insurance decision relies on your health and risk view. Consider your family's needs carefully. This shields you from rising medical costs.

To get good coverage, compare plans. Look at your choices closely. This helps ensure peace of mind for your future.

Frequently Asked Questions

What are the disadvantages of super top up health insurance?

The main downside is that the deductible amount isn't covered. You'll typically need to pay this initial sum yourself, either out of pocket or from your existing base policy, before your highly top-up plan activates. It only steps in for medical expenses that exceed this pre-defined limit within a policy year (this can vary).

Confused between health insurance plans?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

What is the age limit for top-up health insurance?

Entry for top-up health insurance typically begins at 18 years. Most plans offer lifelong renewability once you've purchased it, meaning there's usually no upper age limit for continuing the policy. Some insurers might have a cap for initial buy (do confirm with your chosen provider), but lifelong renewal is quite common.

How to claim super top up?

You claim your highly top-up once medical expenses exceed the deductible amount (typically covered by your base policy). Afterwards, you'll need to submit the remaining hospitalisation bills to your highly top-up insurer. Make sure to provide all necessary documents, including the discharge summary and proof of your base policy's claim settlement.

Can I buy a top-up plan from a different insurer than my base policy?

You can absolutely buy a highly top-up plan from a different insurer than your base policy. These are separate contracts, and IRDAI regulations actually allow this flexibility. Typically, your highly top-up's deductible needs to be exhausted first from your base policy or out-of-pocket expenses (it's how these plans are designed).

Do top-up and super top-up plans cover pre-existing conditions?

Top-up and highly top-up plans generally cover pre-existing conditions. However, coverage only kicks in after a waiting period, typically between 2 to 4 years (this varies by insurer and policy). Your policy document will specify the exact duration; you'll need to complete it before any claims related to a pre-existing condition are processed.

Are top-up plans a good option for senior citizens?

Top-up plans are an excellent choice for senior citizens. They bolster an existing base health policy, providing crucial additional cover when medical bills exceed that primary sum (especially important with rising healthcare costs). You'll typically find premiums much more affordable than buying a brand-new, high-sum insured policy. It's also eligible for tax benefits under Section 80D.

Can a super top-up plan be used with a family floater policy?

You can definitely use a highly top-up plan with your family floater policy. This combination works very well, as the highly top-up's deductible is typically met by your existing floater's sum insured. It's a smart way to boost your family's overall coverage against larger claims (always check policy terms for specifics). This ensures extended protection once the base policy limit runs out.

Written By

Raj Shankar![]()

Principal Officer and General Manager at CoverTiger

With over 7 years of experience in the insurance and fintech industry, Raj Shankar has helped 10,000+ customers secure their families with the right insurance solutions. He has worked with leading brands such as Policybazaar, INDmoney, and CoverTiger, building strong expertise in health insurance, life insurance, sales leadership, and customer advisory. His mission is to make insurance simpler, more transparent, and accessible for every Indian family.