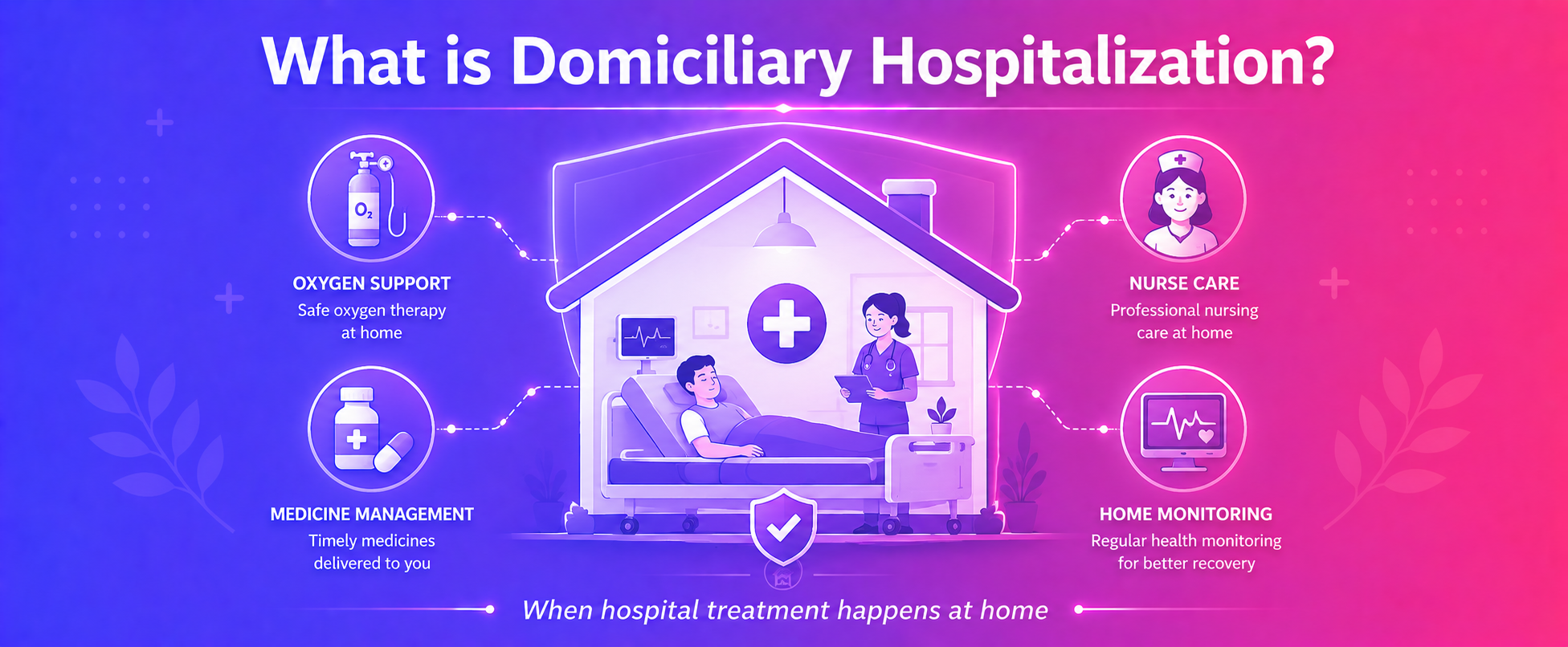

At-home hospitalization means you get medical care at home. This care is for sickness or injuries needing hospital-level attention. Patients receive this treatment where they live. This benefit helps many families across India.

Such a feature is important in certain situations. Sometimes, a sick person cannot travel to a hospital. Other times, hospitals might not have enough beds. Getting medical care at home typically gives good care in a comfortable place. It also helps cover home care costs that often go unpaid.

This guide will explain at-home hospitalization fully. We will cover its meaning, its key advantages, who can use it, and how to get your full claim.

What is domiciliary hospitalisation in health insurance?

At-home hospitalization means you receive medical treatment at home. This is for an illness or injury. Normally, you would need to stay in a hospital for such care. This home treatment offers a choice in your health insurance plan. It replaces a typical hospital stay where you sleep overnight. Many health plans offer domiciliary hospitalization cover for such needs.

In health insurance, at-home treatment covers certain medical services. A doctor must confirm you need these services. You then get this care right at home. These services are for times when a hospital stay is usually required.

To claim domiciliary hospitalization benefits, you typically need to meet specific conditions:

- The patient's health condition makes moving them to a hospital unsafe.

- Or, no hospital beds are free in local hospitals at that time.

- A doctor must actively watch over your home treatment.

- This care often needs to last for at least 3 full days, which is 72 hours.

At-home hospitalization cover helps you in these situations. It usually does not include general home nursing or just recovery help. A doctor must order care that is similar to what you would get in a hospital. These domiciliary hospitalization benefits can help you get good medical care when you cannot go to a hospital.

When does domiciliary hospitalization get covered and what are the eligibility criteria?

To get home hospital care (at-home hospitalization) paid for, you must meet certain rules. Your policy will not cover all home medical care.

First, a doctor needs to suggest home treatment. This written note should say you need hospital-level care at home.

Also, your health must make going to a hospital unsafe. For example, if you have very bad broken bones or are getting better from a big surgery, moving you could make you sicker. These situations often let you get at-home hospital benefits.

Sometimes, a hospital bed is just not open. When local hospitals are full, you might get treatment at home. Insurance companies may ask for proof that no beds are free.

Remember, your plan usually does not pay for home treatment just because it's easier. This is true if hospital beds are open and you can travel. Always read all the rules and details of your policy.

What domiciliary hospitalization cover includes and what it leaves out:

What Is Included

at-home hospitalization covers medical costs. This is for treatment you get while at home. Such care must replace a hospital stay. It often includes doctor's fees and nursing help. Medicines and tests done at home are also typically paid for. Your insurance papers list the specific illnesses covered.

What Is Not Included

General home nursing or rest cures are usually not covered. This plan does not pay for conditions that don't need hospital care. Also, medicines you prescribe for yourself are not included. Cosmetic treatments are often left out. Always check your policy for a full list of what is not covered.

Confused between health insurance plans?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

What medical expenses are typically included?

At-home hospitalization helps pay some medical bills. This happens if you get hospital-like care at home. You do not actually stay in a hospital. This plan helps cover the treatment you need outside a hospital.

To get this benefit, a doctor must give you a medical necessity certificate. This paper shows you need home treatment. In most cases, this coverage pays you back for costs. It pays up to your plan’s total limit.

Key costs often included:

* Cost of medicines and drugs your doctor orders.

* Fees for doctor visits.

* Charges for nurses who care for you.

* Costs for any tests done at home.

* Costs of medical equipment, like oxygen tanks.

What is commonly excluded from coverage?

It is important to know what your health plan will not pay for in home hospital claims. This benefit covers some treatments you get at home. It lets you get care at home instead of staying in a hospital. Knowing what is not covered helps you understand your health plan.

Home hospital care usually does not pay for these common things:

- Any treatment at home that lasts less than 72 hours straight.

- Costs for medical care before or after your home hospital treatment.

- Help that is not medical, like support for bathing or eating.

- Certain sicknesses, such as asthma, diabetes, or mental health problems.

- Other kinds of treatments like Ayurveda, Yoga, or Homeopathy (AYUSH) are usually not paid for.

Domiciliary hospitalization benefits

What are the benefits of at-home hospitalization cover? This option offers many good points for patients and their families.

• Improved Patient Comfort and Healing: Receiving medical care at home brings great comfort. Patients stay in a familiar place. Being close to family often boosts mental well-being. This setup can help people heal well.

• Lower Overall Cost: at-home hospitalization typically cuts down treatment expenses. It removes costs like hospital room rent. Other standard hospital fees are also avoided. This makes medical care more affordable for many.

• The risk of infections is much lower at home. Hospitals can sometimes expose patients to more germs. This is very good for people with weak immune systems.

• Focused Medical Attention: Patients often get very personal care at home. Nurses and doctors can give direct, one-on-one attention. This kind of focused support is often hard to get on a busy hospital ward.

• Family members find it easier to provide support. They do not face strict hospital visiting hours. This convenience lets families offer ongoing care and help.

Confused between health insurance plans?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

Domiciliary hospitalization vs. home care: what's the difference?

Many people often ask about the difference between home care and at-home treatment. They also want to know if home care is the same as at-home hospitalization. These two types of care given at home are not the same.

at-home hospitalization, also known as domiciliary hospitalization, happens when a patient needs hospital-level treatment. However, this care cannot be given in a hospital. This can happen if there are no hospital beds available. Or the patient has special health needs. It could also be to avoid infection risks. A trained doctor must confirm that strong medical treatment is needed. This treatment would usually only be done inside a hospital. This type of serious medical care at home involves active treatment. Many health insurance plans call it a "defined benefit." Some Indian companies, like Star Health or Niva Bupa, do provide it.

Home care, on the other hand, usually helps you get better after leaving the hospital. It also helps manage long-term sickness. This care can include nursing help, physical therapy, or help with daily tasks. Home care generally gives supportive or basic help. It does not replace an active

hospital stay. Insurance plans often do not cover general home care. Coverage is usually only for getting better after surgery or for certain health problems.

How to claim domiciliary treatment in health insurance

For people with insurance, knowing how to claim for at-home hospitalization is important. What is the process for a at-home claim? Here is how you can claim for home hospitalization.

1. Doctor's Recommendation

First, a doctor must suggest home hospitalization. They will confirm your need for medical care at home.

2. Inform Your Insurer

Tell your insurance company quickly. This usually means within 24 to 72 hours of the doctor's advice. Provide details about the estimated costs for your home care.

3. Send Documents

Gather all necessary papers and submit them. These include your doctor's prescriptions and medical reports. You will also need bills for doctor visits and nursing care at home.

4. Claim Review

The insurance company will check the documents you send. If they approve, they will pay for your treatment costs. This payment always follows your specific policy rules.

How to find health insurance with domiciliary hospitalization cover

When you look for health insurance, check carefully for at-home hospitalization cover. Not all health plans include this benefit automatically. Some Indian insurance companies offer it as a standard part of their plans. For other plans, you might need to buy it as an extra option.

Always read the policy details and brochure before you buy. Look for the words 'at-home Hospitalization'. This confirms what the policy offers for home treatment.

You can use comparison websites for insurance online. Many sites, like Cover Tiger, let you filter plans. You can search for policies with at-home hospitalization instead of just hospital stays. This helps make finding the right plan simpler.

Once you find a policy with this cover, check its sub-limit. Many insurers cap the money they pay for home care. This might be a fixed amount or a percentage of your total sum insured, typically 10%. Knowing these limits helps avoid surprises when you make a claim. Also, watch out for any policy exclusions.

Conclusion

Confused between health insurance plans?

Let AI decide for you.

- AI compares 30+ insurers

- No sales pressure

- Result in 60 seconds

- 100% free

No spam. No calls unless you want them.

At-home hospitalization is a good health insurance benefit. It gives an important safety net. This benefit typically covers medical care. It is much like hospital care, but you get it at home. Sometimes, this can be a better choice than going to a hospital. It helps patients who need steady treatment at home, often for long illnesses.

You must fully understand your health insurance papers. Always check the specific rules carefully. See what your plan covers and what it does not for this type of care. Different Indian insurance companies may have varied rules for at-home care.

Think about your family's unique health needs. Try to find a health insurance plan that includes at-home hospitalization. This offers you complete financial protection. Knowing these important features helps you use your health policy well.

Frequently Asked Questions

Q: What is the domiciliary limit?

The at-home limit defines the maximum amount your health insurance will cover for medical treatment received at home. It's typically a specific sub-limit within your overall sum insured. Insurers generally set this as a fixed percentage or a monetary cap (check your policy document), governed by IRDAI guidelines for Indian plans.

Q: Can I claim for domiciliary hospitalization yes or no?

You can claim for at-home hospitalization only if your health insurance policy just for includes this benefit. It's typically for conditions that would otherwise require hospital admission, but treatment is provided at home (this needs proper medical certification). Your policy document, regulated by IRDAI, details the specific terms.

Q: What is the minimum duration for domiciliary treatment?

Typically, most Indian health insurance policies require a minimum of three consecutive days for at-home treatment coverage. It's often a full 72 hours (this can vary slightly depending on your insurer). You'll always need to check your specific policy wording, as each plan has its own conditions.

Q: Is there any waiting period for domiciliary hospitalization?

Yes, at-home hospitalization cover usually comes with waiting periods. You'll typically see an initial period, often 30 days from policy inception, and specific waiting periods for pre-existing conditions (this can range from two to four years, depending on your insurer). Always review your policy wording for the precise timelines.

Q: Are pre- and post-hospitalization expenses covered with domiciliary treatment?

Yes, most Indian health policies do cover pre and post-hospitalization costs for at-home treatment, provided the at-home claim itself is admissible. These expenses, such as diagnostic

tests or follow-up medications, are typically reimbursed. Just check your policy wording carefully, as it's always subject to specific terms and sub-limits (this can vary).

Q: Is a cashless facility available for domiciliary hospitalization?

A cashless facility isn't typically available for at-home hospitalization here in India. Most claims are processed on a reimbursement basis; you pay first, then submit documents to your insurer. A few specific plans might offer cashless options through empaneled home healthcare providers (this can vary). Always check your individual policy for exact terms.

Q: Is there a maximum number of days for which domiciliary hospitalization is covered?

at-home hospitalization usually has a maximum number of days covered per policy year. You'll typically see limits ranging from 7 to 30 days, though this really depends on your specific health plan. It's always best to check your policy wording for the exact duration and terms (insurers do set these individually).

Q: What should I do if my domiciliary claim is rejected?

First, carefully review the rejection letter from your insurer; it will clearly state the reason for denial. Then, contact their customer service to understand why, and typically, they'll ask for additional documents or clarification (keep copies of everything). If that does not resolve the matter, use their internal grievance process, or escalate to IRDAI's Bima Bharosa portal.

Written By

Raj Shankar![]()

Principal Officer and General Manager at CoverTiger

With over 7 years of experience in the insurance and fintech industry, Raj Shankar has helped 10,000+ customers secure their families with the right insurance solutions. He has worked with leading brands such as Policybazaar, INDmoney, and CoverTiger, building strong expertise in health insurance, life insurance, sales leadership, and customer advisory. His mission is to make insurance simpler, more transparent, and accessible for every Indian family.